Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

Trump Admin's $950 Million Bet on Oil Price Plunge Before Ceasefire Turned Crude Market into Insider Trading Heaven

On Tuesday, April 7, 2026, at 19:45 GMT, just under three hours from when Trump announced the U.S.-Iran "two-week ceasefire" on Truth Social, a London trader was logging off while Asian traders were not yet in. Typically, only a few hundred contracts of crude oil futures would change hands in a minute during this lull period. However, during this hour, someone unloaded approximately 6,200 lots of Brent crude oil and 2,400 lots of WTI crude oil futures in quick succession, totaling 8,600 lots with a notional value of around $950 million.

The next day, as the Asian session opened, crude oil prices plummeted by about 15%, with WTI dropping below $100. According to Reuters citing LSEG's transaction data, the scale of this short position was "entirely atypical for that time window." Congressman Ritchie Torres penned a letter to the U.S. SEC and CFTC on April 8, requesting an investigation.

This wasn't the first time. More precisely, it was the second recorded instance of the same "playbook" amid the U.S.-Iran conflict.

The same trading signature, hitting the mark twice

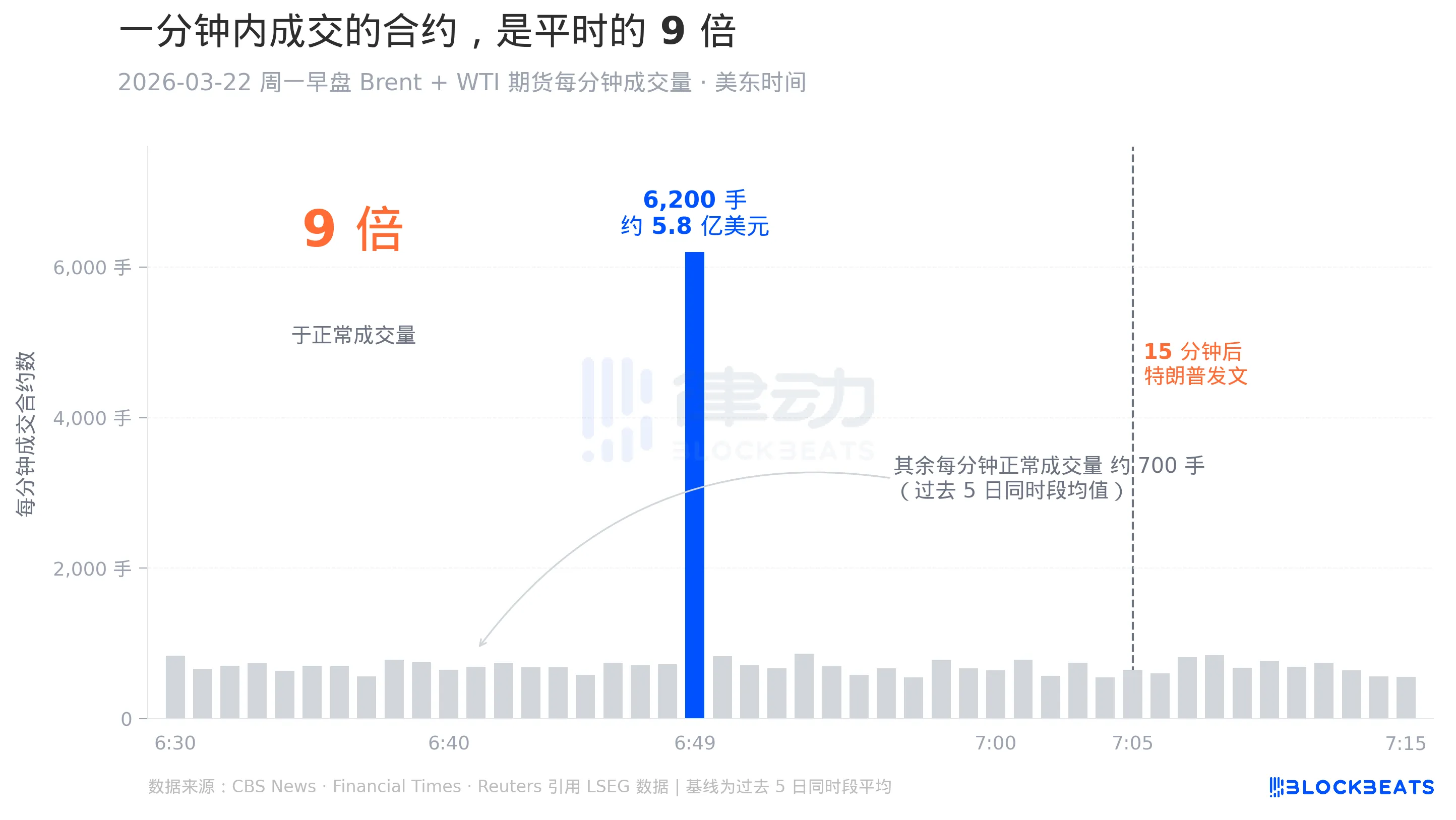

The earlier instance on Monday morning, March 22, 2026, didn't gain the same notoriety as the April 7 event because it didn't cause a significant price drop. However, structurally, it was the prototype of this "playbook." As per CBS News and Financial Times-cited trading data, between 6:49 and 6:50 Eastern Time, or 10:49 GMT, a total of 6,200 lots of Brent and WTI futures were traded, amounting to around $580 million.

Fifteen minutes later, Trump posted on Truth Social, stating he was engaged in "constructive dialogue" with Iran and postponing the planned strike on Iranian energy facilities by five days. Crude oil prices plunged that day, the S&P 500 surged, and the Dow gained over 1,000 points in a single day.

Aligning the timelines of these two events reveals a detail: the "Brent leg" within that 8,600-lot position on April 7 was also exactly 6,200 lots. The repetition of the same number in two entirely different time frames could be a coincidence or an indication of identical position sizing. In trading circles, this type of repetition is called a "signature," referring to a group of traders following a predetermined formula. CBS's report cited two unnamed former CFTC investigators stating that this precise repetition "itself is an investigative signal."

9x the Norm, Happening in an Hour No One Was Watching

Many of the first readers who saw this news thought 19:45 GMT was a "closed market period." It was not. Brent crude oil futures trade almost 24 hours electronically, with only a brief shutdown on weekends. 19:45 GMT marks a more subtle moment. The previous minute (19:28 to 19:30 London time) had just concluded the day's "settlement window," the two minutes the exchange uses to determine the official daily settlement price.

As soon as the settlement window closes, most European professional traders are off work. The Asian trading desks in Tokyo and Singapore won't come online for several hours. This one-hour period is usually one of the least liquid windows of the day. According to ICE's official product specs, Brent's true peak trading volume occurs during the European day session.

If we zoom in on the anomaly of that minute on March 22 and compare, the difference becomes more apparent. According to CBS citing LSEG trade details, the normal trading volume for each minute around that time for the previous and following five days was about 700 contracts. That minute saw 6,200 contracts traded, nearly 9 times the usual amount. The blue bar in the chart represents that minute, while the other gray bars before and after are from the same hour, densely packed at the bottom.

The significance of this comparison is that the 9x surge did not happen during the most liquid trading hours but was concentrated in the thinnest minute of the order book. When writing about this on his Substack, Paul Krugman used a metaphor, saying it was like "honking your horn with no one around on a deserted street at night," either not caring if anyone hears or having a specific reason for acting at that moment.

Three Consistent Trades

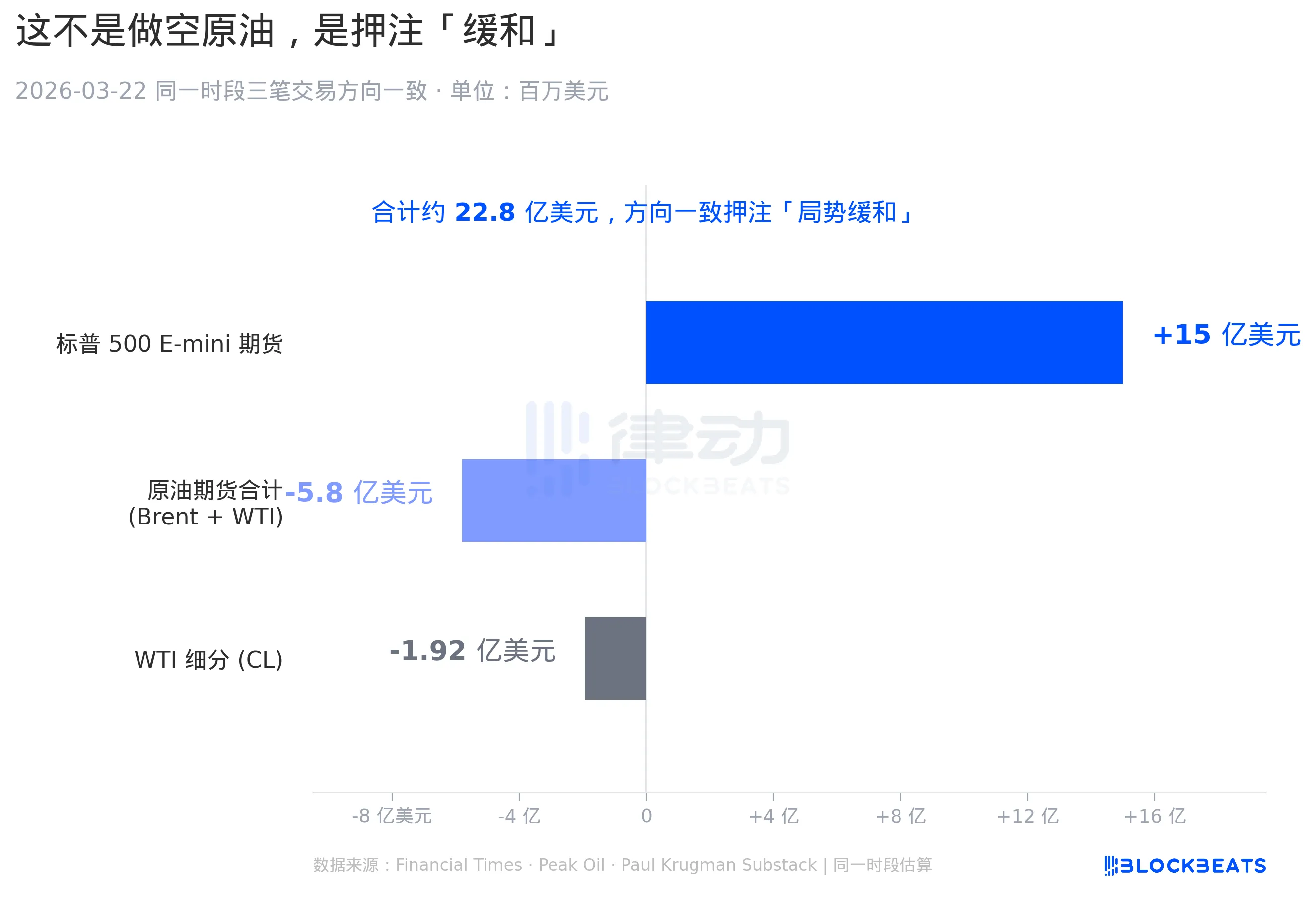

This chart shows the other half of the anomaly on March 22 that many reports overlooked. In follow-up articles at the end of March, the Financial Times and Peak Oil mentioned that during the same period as the $580 million crude oil short, there were two other consistent trades: a buy order of approximately $1.5 billion in S&P 500 E-mini futures and an independent short of $192 million on WTI (CL contract).

The "S&P 500 E-mini futures" are the most active stock index futures contract on the exchange, with one contract equating to around $250,000 worth of the S&P 500 index. It is a standard tool for institutions to hedge against the overall direction of the US stock market. "Buying E-mini" is a bet on the US stock market's rise. The "WTI specific short" is an additional short position taken on another futures product line for crude oil (WTI traded in the US). Together, these three trades amounted to a nominal value of around $2.28 billion.

Looking at these three trades together, they appear more like a paired trade, betting on the same macro scenario, which is the easing of US-Iran tensions. How would easing affect the market? The oil supply panic subsides, leading to a fall in oil prices. Geopolitical risk premium diminishes, resulting in a stock market rebound. Combining these three positions creates the cleanest profit combination in this scenario. To paraphrase Paul Krugman, "If you know you will see the words 'constructive dialogue' two hours later, these are the three trades you would make."

The Same Script, Also Seen in Prediction Markets

Shifting focus from the futures market to the crypto world's prediction market Polymarket reveals an almost identical mirror image.

Polymarket is a binary prediction market platform built on Ethereum, where users bet on whether an event will occur, with odds determined by market participants themselves. After the event's outcome is confirmed, winners receive a payout. All its transactions are on-chain, and anyone can view the history of each wallet.

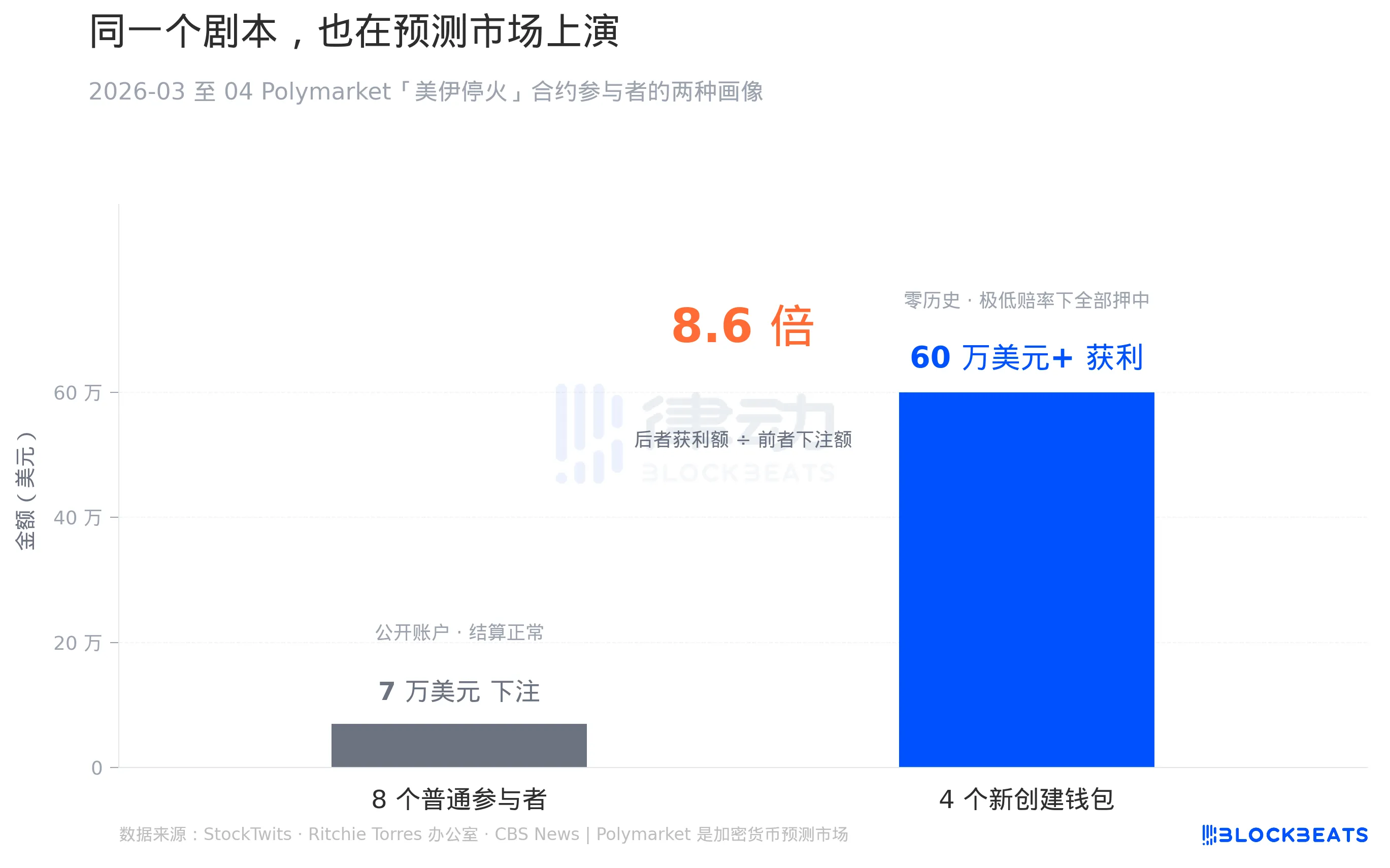

According to on-chain data cited by StockTwits, in the final week of the "Will there be a ceasefire between the US and Iran within 30 days on Polymarket" contract, there were 8 accounts with a "normal profile," all being publicly known old accounts, collectively wagering around $70,000. There were wins and losses, and the settlement process had no suspicious points. However, at the same time, 4 other accounts had completely different profiles. These 4 wallets were newly created just before the event, with no prior on-chain transaction history. Their first action upon entry was to heavily bet on "there will be a ceasefire" at very low odds, and in the end, they all won, collectively making over $600,000 in profit.

From $70,000 to $600,000, the multiplier in between is 8.6 times, with the latter's profit being nearly nine times the total amount wagered by the former. According to Polymarket's own settlement rules, the winner's amount = bet amount × reciprocal of odds. To earn $600,000 in a week, these 4 wallets either placed a heavy bet at a very low odds point (indicating a high market belief in "no ceasefire"), or they diversified their bets multiple times, with on-chain data indicating the former.

Ritchie Torres's office mentioned this detail in a letter to the SEC and CFTC, aligning it with the anomalous behavior in crude oil futures as evidence of a "cross-market synchronous signal." This is why Torres already introduced legislation against insider trading in prediction markets around the end of March. For him, the crude oil futures side was not an isolated incident.

Will There Really Be an Investigation?

Let's first examine the reality at the federal level. According to the SEC's Enforcement Report for FY 2025 released in early April, the past year saw 313 new SEC enforcement actions, the lowest point in the past decade, a 27% decrease from the 583 cases in FY 2024. On the CFTC side, there was no simultaneous release of an equivalent annual report, but in early April, the law firms Sullivan & Cromwell and Skadden, which track CFTC enforcement trends, noted in their comments that the CFTC's enforcement division had significantly slowed down at the beginning of 2025.

However, just about a week before Torres wrote his letter, the CFTC had announced the 5 key enforcement priorities for FY 2026. According to Sullivan & Cromwell's analysis, the top priority is "Insider Trading, including Market Manipulation," and the second is "Market Manipulation, particularly in the energy markets."

The subtlety here lies in the fact that the CFTC itself verbally placed this issue at the top priority, but historically, the CFTC has initiated very few cases of the type of "single unusual trade" in the futures markets. The significant energy market cases that have been successfully prosecuted in the past, such as the penalties against Trafigura, Freepoint, and TotalEnergies in 2024, were all off-exchange long-term manipulation cases with a duration of 2 to 4 years, not targeting a one-time abnormal short position on the market.

Another line of investigation that could potentially yield results is related to the actions of New York State Attorney General Letitia James. Starting in April 2025, she has been using New York's Martin Act to track a series of "timely, high-return trades related to public statements by Trump."

The Martin Act is New York's securities anti-fraud law, and it has a key feature that federal law lacks: the prosecution does not need to prove that the defendant subjectively intended to defraud, but only that the trading behavior itself objectively exhibits fraudulent characteristics, in order to bring charges. For events like "precise lurking," proving subjective intent is precisely the most challenging aspect in federal insider trading cases.

You may also like

Prediction Markets Under Bias

Stolen: $290 million, Three Parties Refusing to Acknowledge, Who Should Foot the Bill for the KelpDAO Incident Resolution?

ASTEROID Pumped 10,000x in Three Days, Is Meme Season Back on Ethereum?

ChainCatcher Hong Kong Themed Forum Highlights: Decoding the Growth Engine Under the Integration of Crypto Assets and Smart Economy

Why can this institution still grow by 150% when the scale of leading crypto VCs has shrunk significantly?

Anthropic's $1 trillion, compared to DeepSeek's $100 billion

Geopolitical Risk Persists, Is Bitcoin Becoming a Key Barometer?

Annualized 11.5%, Wall Street Buzzing: Is MicroStrategy's STRC Bitcoin's Savior or Destroyer?

An Obscure Open Source AI Tool Alerted on Kelp DAO's $292 million Bug 12 Days Ago

Mixin has launched USTD-margined perpetual contracts, bringing derivative trading into the chat scene.

The privacy-focused crypto wallet Mixin announced today the launch of its U-based perpetual contract (a derivative priced in USDT). Unlike traditional exchanges, Mixin has taken a new approach by "liberating" derivative trading from isolated matching engines and embedding it into the instant messaging environment.

Users can directly open positions within the app with leverage of up to 200x, while sharing positions, discussing strategies, and copy trading within private communities. Trading, social interaction, and asset management are integrated into the same interface.

Based on its non-custodial architecture, Mixin has eliminated friction from the traditional onboarding process, allowing users to participate in perpetual contract trading without identity verification.

The trading process has been streamlined into five steps:

· Choose the trading asset

· Select long or short

· Input position size and leverage

· Confirm order details

· Confirm and open the position

The interface provides real-time visualization of price, position, and profit and loss (PnL), allowing users to complete trades without switching between multiple modules.

Mixin has directly integrated social features into the derivative trading environment. Users can create private trading communities and interact around real-time positions:

· End-to-end encrypted private groups supporting up to 1024 members

· End-to-end encrypted voice communication

· One-click position sharing

· One-click trade copying

On the execution side, Mixin aggregates liquidity from multiple sources and accesses decentralized protocol and external market liquidity through a unified trading interface.

By combining social interaction with trade execution, Mixin enables users to collaborate, share, and execute trading strategies instantly within the same environment.

Mixin has also introduced a referral incentive system based on trading behavior:

· Users can join with an invite code

· Up to 60% of trading fees as referral rewards

· Incentive mechanism designed for long-term, sustainable earnings

This model aims to drive user-driven network expansion and organic growth.

Mixin's derivative transactions are built on top of its existing self-custody wallet infrastructure, with core features including:

· Separation of transaction account and asset storage

· User full control over assets

· Platform does not custody user funds

· Built-in privacy mechanisms to reduce data exposure

The system aims to strike a balance between transaction efficiency, asset security, and privacy protection.

Against the background of perpetual contracts becoming a mainstream trading tool, Mixin is exploring a different development direction by lowering barriers, enhancing social and privacy attributes.

The platform does not only view transactions as execution actions but positions them as a networked activity: transactions have social attributes, strategies can be shared, and relationships between individuals also become part of the financial system.

Mixin's design is based on a user-initiated, user-controlled model. The platform neither custodies assets nor executes transactions on behalf of users.

This model aligns with a statement issued by the U.S. Securities and Exchange Commission (SEC) on April 13, 2026, titled "Staff Statement on Whether Partial User Interface Used in Preparing Cryptocurrency Securities Transactions May Require Broker-Dealer Registration."

The statement indicates that, under the premise where transactions are entirely initiated and controlled by users, non-custodial service providers that offer neutral interfaces may not need to register as broker-dealers or exchanges.

Mixin is a decentralized, self-custodial privacy wallet designed to provide secure and efficient digital asset management services.

Its core capabilities include:

· Aggregation: integrating multi-chain assets and routing between different transaction paths to simplify user operations

· High liquidity access: connecting to various liquidity sources, including decentralized protocols and external markets

· Decentralization: achieving full user control over assets without relying on custodial intermediaries

· Privacy protection: safeguarding assets and data through MPC, CryptoNote, and end-to-end encrypted communication

Mixin has been in operation for over 8 years, supporting over 40 blockchains and more than 10,000 assets, with a global user base exceeding 10 million and an on-chain self-custodied asset scale of over $1 billion.

$600 million stolen in 20 days, ushering in the era of AI hackers in the crypto world

Vitalik's 2026 Hong Kong Web3 Summit Speech: Ethereum's Ultimate Vision as the "World Computer" and Future Roadmap

On the same day Aave introduced rsETH, why did Spark decide to exit?

Full Post-Mortem of the KelpDAO Incident: Why Did Aave, Which Was Not Compromised, End Up in Crisis Situation?

After a $290 million DeFi liquidation, is the security promise still there?

ZachXBT's post ignites RAVE nearing zero, what is the truth behind the insider control?

Vitalik 2026 Hong Kong Web3 Carnival Speech Transcript: We do not compete on speed; security and decentralization are the core