Messari: Trading US Stocks on Perp DEX, the Next New Frontier

Original Article Title: Equity Perps: Tall Orders and Slow Beginnings

Original Article Author: Sam, Messari Research

Original Article Translation: Deep Tide TechFlow

Key Insights:

Equity perpetual contracts still belong to a high-potential but unproven area, with limited appeal in the on-chain market mainly due to misaligned audience, weak demand, and more popular alternatives (such as 0DTE options).

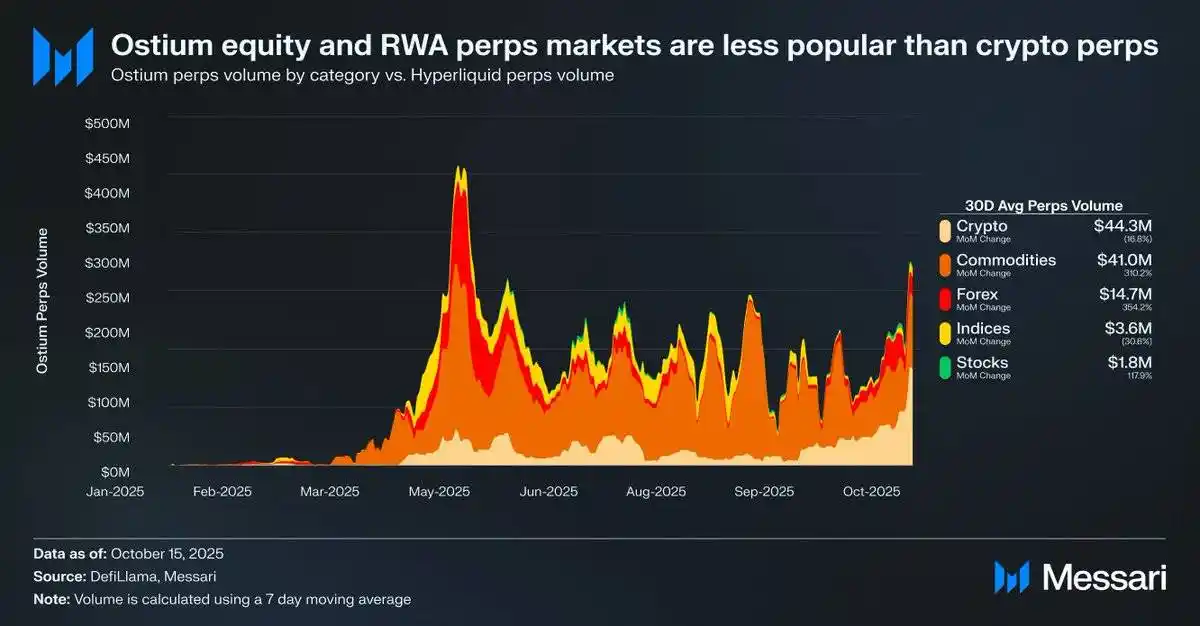

For example, the daily average trading volume of equity perpetual contracts on the Ostium platform is only $1.8 million, while cryptocurrency perpetual contracts reach as high as $44.3 million, demonstrating a weak market demand.

This may imply that due to infrastructure and regulatory constraints, market demand has not been fully unleashed. Hyperliquid's recent HIP-3 upgrade has provided the best opportunity for equity perpetual contracts, but the adoption process is expected to be gradual.

Source: Messari (@0xCryptoSam)

Equity perpetual contracts are considered the inevitable next blue ocean in the on-chain market, but current data suggests that this area is still challenging to break through in the short term. Ostium, as a decentralized exchange focusing on real-world assets (RWAs), has a daily average trading volume of equity perpetual contracts of only $1.8 million, while cryptocurrency perpetual contracts reach $44.3 million, reflecting weak demand.

This adoption gap is mainly due to misaligned audience. On-chain traders have little interest in stocks, while off-chain platforms (such as Robinhood) allow traders to easily trade stocks and options but not perpetual contracts. International investors may be a potential target audience as they cannot directly access the US stock market. However, these investors may prefer to hold stocks directly to gain shareholder rights while avoiding funding costs and settlement risks.

Compared to tokens, stocks have fewer interoperability challenges, benefiting from the convenience of synthetic wrapping. For the average investor, almost every stock in the global market has already been abstracted through the search bar's individual stock code. Therefore, even though perpetual contracts add permissionless and censorship-resistant features to stocks, ordinary stock investors are either unaware of this or simply not interested.

Source: fow

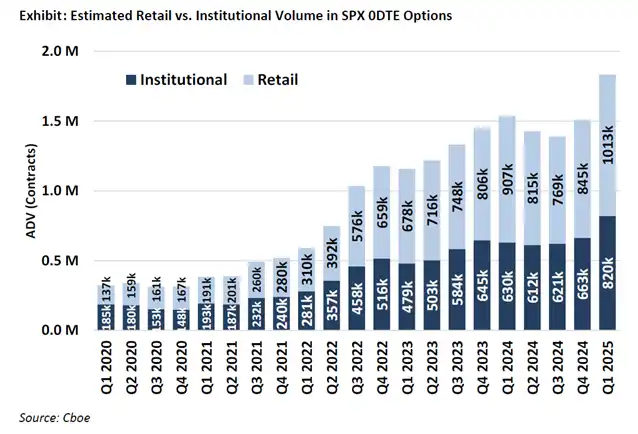

The most likely users of stock perpetual contracts are retail options traders (who drive 50%-60% of 0DTE trades on the Robinhood platform). However, traditional exchanges relying on banking services will only adopt stock perpetual contracts when the law is clear. The U.S. Commodity Futures Trading Commission (CFTC) has approved perpetual contract trading for BTC and ETH, but these two have been deemed non-securities. While perpetual contracts are more intuitive than options, the popularization of stock perpetual contracts may be slower than expected due to the close link between retail adoption paths and legal clarity.

Source: @Kaleb0x

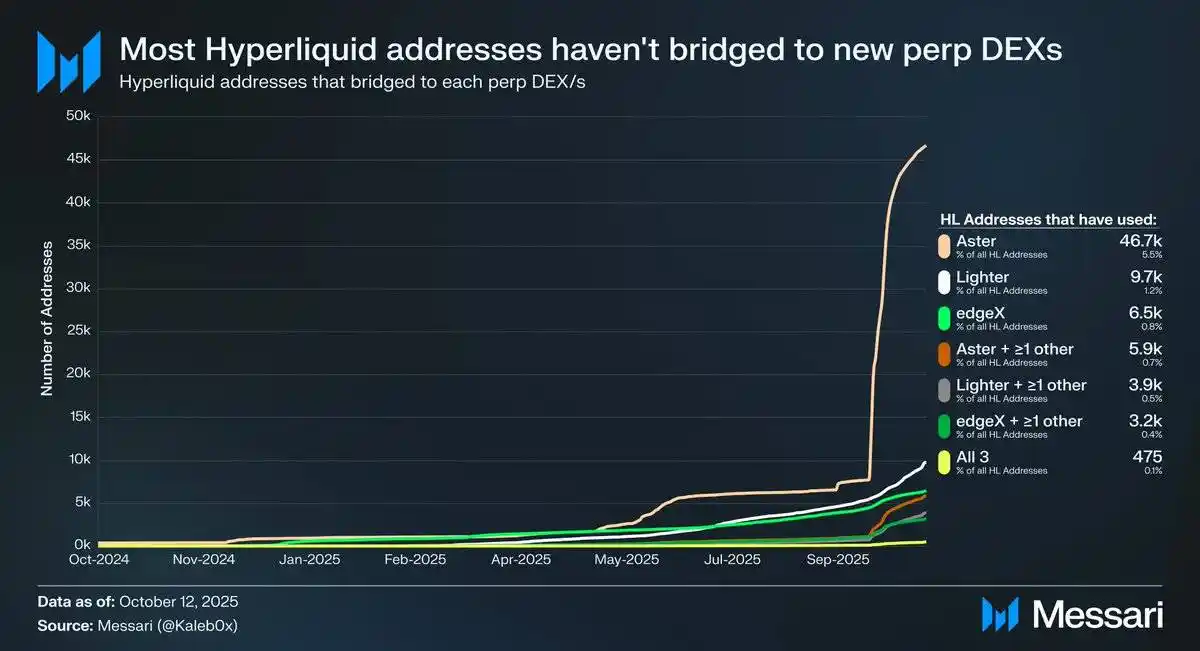

Let's discuss the potential development direction of stock perpetual contracts under the background of the HIP-3 upgrade on Hyperliquid. HIP-3 introduces a permissionless perpetual contract market, and data shows that less than 10% of Hyperliquid addresses have bridged to Aster, Lighter, and edgeX, with even fewer users opting for multiple perpetual contract decentralized exchange (DEX) platforms. This indicates that funds on Hyperliquid are sticky and of higher quality. Based on this data, the future of stock perpetual contracts can be predicted from two perspectives:

Hyperliquid users are loyal to the platform and, regardless of asset listings or features, they are more likely to choose Hyperliquid over other perpetual contract DEXs.

Hyperliquid users are satisfied with the current perpetual contract market products.

I believe both of these viewpoints make sense. Considering that Hyperliquid users have not massively shifted funds in the face of incentives, they may be loyal to Hyperliquid. However, as most of the trading volume and open interest on Hyperliquid are concentrated in mainstream assets, similar to other perpetual contract DEXs, it is currently difficult to determine whether Hyperliquid users care about market diversity and whether stock perpetual contracts are attractive to regular users (more importantly, to the whales holding 70% of Hyperliquid's open interest).

In addition, these traders may also have accounts on both traditional trading platforms and brokerage platforms, further limiting the potential market size of stock perpetual contracts on Hyperliquid.

It is worth noting that stock perpetual contracts may not bring new open interest or trading volume to Hyperliquid but may instead divert existing trading volume.

Although Ostium (with an annual average perpetual contract trading volume of $220 billion) and stock tokenization tools (such as xStocks, with a spot trading volume of $2.79 billion) have not yet experienced explosive growth, this may reflect infrastructure limitations rather than a lack of underlying demand. This pattern mirrors the early growth trajectory of perpetual contracts. GMX demonstrated the demand for on-chain perpetual contract markets, but the infrastructure at the time could not support sustained trading volume. Hyperliquid overcame this bottleneck, unleashing latent demand. By the same logic, after stock perpetual contracts receive the necessary performance and liquidity enhancements under HIP-3, they may find their first scalable product-market fit on Hyperliquid. While current data cannot confirm this outcome, this precedent is worth noting.

Compared to 0DTE options, the long-term potential of stock perpetual contracts remains evident. Projects like Trade[XYZ] can leverage regulatory arbitrage to build an early user base before entering the market on traditional exchanges. However, the real challenge lies in attracting off-chain retail traders, which has always been difficult for crypto applications.

You may also like

Kalshi Executive Challenges “SBF Backed AI Unicorns” Narrative, Says Leopold Aschenbrenner Was Key Figure

Kalshi executive John Wang questioned the “SBF backed AI unicorns” narrative, saying Leopold Aschenbrenner was the key figure behind major AI investment decisions.

Pantera Capital Partner: How Tokenization is Restructuring the Private Equity and Early Investment Ecosystem?

New York Proposes Stricter Stablecoin Issuer Rules Aligned With Federal GENIUS Act

NYDFS proposed stricter stablecoin issuer rules aligned with the GENIUS Act, covering reserves, custody, redemption timelines, audits, and capital buffers.

Every exchange is a "Universal Exchange."

The counterattack of traditional finance: Alliance chains are quietly reviving

CryptoQuant Says Bitcoin Profitable Supply Is Near 45% Pressure Zone as On-Chain Data Points to Market Repricing

CryptoQuant said Bitcoin’s profitable supply is nearing the 45% pressure zone, signaling rising market stress, unrealized losses, and a possible on-chain repricing phase.

Bitcoin Falls Below 200-Week Moving Average as On-Chain Data Shows Over Half of Supply in Loss

Bitcoin dropped below its 200-week moving average as on-chain data showed over 50% of circulating supply is now in loss, signaling rising market stress.

CFTC Reportedly Plans New Prediction Market Rules Focused on Manipulation Risk and Public Interest Review

The CFTC is reportedly preparing new prediction market rules focused on manipulation risk, public interest review, and retail trader protections.

Meet the new WEEX trial fund—your gateway to greater profits

WEEX Labs Lands at Dutch Blockchain Week: A Disruptive Crypto × AI Conversation Sets Sail in Amsterdam

SK Hynix Reportedly Plans U.S. ADR Listing as Early as August, With SEC Approval Possible in Late June

SK Hynix may pursue a U.S. ADR listing as early as August, with SEC approval reportedly possible in late June amid strong AI chip supply chain demand.

SpaceX vs Tesla vs xAI: Which Elon Musk Trade Has the Biggest Upside in 2026?

OpenAI Reveals It Has Confidentially Submitted an S-1 to the SEC, Keeping the Door Open for a Future IPO

On June 9, according to an OpenAI announcement, the company recently confidentially submitted a draft S-1 registration statement to the U.S. Securities and Exchange Commission (SEC), beginning the preliminary compliance process for a potential initial public offering. OpenAI said it chose to disclose this proactively because it expected the news might leak; however, the company has not yet set a specific listing timeline, and related arrangements may still take some time.

Latest research from 13 top universities including Cornell University: The current state, challenges, and misconceptions of the fusion of Crypto and AI

Deconstructing Anthropic: The Best AI Company, Possibly Also a Type of Organizational Invention

Apollo and Blackstone Reportedly Back $35 Billion Anthropic Chip Financing as Deal Details Remain Unclear

On June 9, according to currently available news alerts, Apollo and Blackstone Group participated in a $35 billion financing for an Anthropic “chip project.” Based on the original wording of the report, the funding has already been raised, but public information remains limited. The financing structure, use of proceeds, project entity, and whether Apollo and Blackstone participated through equity, debt, or project financing have not yet been disclosed.

Humanity Protocol Security Incident Escalates: More Than $31 Million Stolen From Related Addresses as Attacker Continues Selling H for ETH

On June 9, according to monitoring by Onchain Lens, more than $31 million has been stolen from addresses linked to Humanity Protocol, and the attack is still ongoing, with the hacker continuously swapping H tokens for ETH. Project founder Terence Kwok later confirmed the security incident on X, saying the issue involved a private key leak.

Bloomberg: As Bitcoin Weakens, Stablecoins and RWA Continue to Drive Expansion in Crypto Businesses

In June, Bloomberg reported that despite Bitcoin falling below $60,000 last week, wiping out about $235 billion in market value within seven days, and dropping close to 50% from last year’s peak, some core businesses in the crypto industry are still expanding, mainly in stablecoins, real-world asset tokenization (RWA), payments, and infrastructure. The report also noted that overall altcoin activity has contracted significantly: altcoin market capitalization has fallen from a peak of about $431 billion in November 2021 to around $170 billion, and among the tens of millions of tokens issued in recent years, fewer than 1,700 still maintain meaningful trading activity.

Kalshi Executive Challenges “SBF Backed AI Unicorns” Narrative, Says Leopold Aschenbrenner Was Key Figure

Kalshi executive John Wang questioned the “SBF backed AI unicorns” narrative, saying Leopold Aschenbrenner was the key figure behind major AI investment decisions.

Pantera Capital Partner: How Tokenization is Restructuring the Private Equity and Early Investment Ecosystem?

New York Proposes Stricter Stablecoin Issuer Rules Aligned With Federal GENIUS Act

NYDFS proposed stricter stablecoin issuer rules aligned with the GENIUS Act, covering reserves, custody, redemption timelines, audits, and capital buffers.

Every exchange is a "Universal Exchange."

The counterattack of traditional finance: Alliance chains are quietly reviving

CryptoQuant Says Bitcoin Profitable Supply Is Near 45% Pressure Zone as On-Chain Data Points to Market Repricing

CryptoQuant said Bitcoin’s profitable supply is nearing the 45% pressure zone, signaling rising market stress, unrealized losses, and a possible on-chain repricing phase.