Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

Market Prediction Fallacy: Is Trading Based on Fact or Rule?

Original Title: "Prediction Market Plunged into Another Major Controversy: Are You Trading on Fact or Rule?"

Original Author: Asher, Odaily Planet Daily

The prediction market can be said to be the most hotly debated track in the current Web3 discussion.

Prediction trading around macro events, the crypto industry, and even entertainment topics continues to heat up, with the level of discussion and participation constantly rising. However, as the market rapidly develops, some discordant voices have gradually emerged—certain events have deviated from users' expectations based on common sense or "real-world understanding" at settlement, triggering controversies regarding rule design, fairness, and platform credibility.

Recently, the prediction market has seen two consecutive high-controversy events. Below, the Odaily Planet Daily will sort out and discuss them.

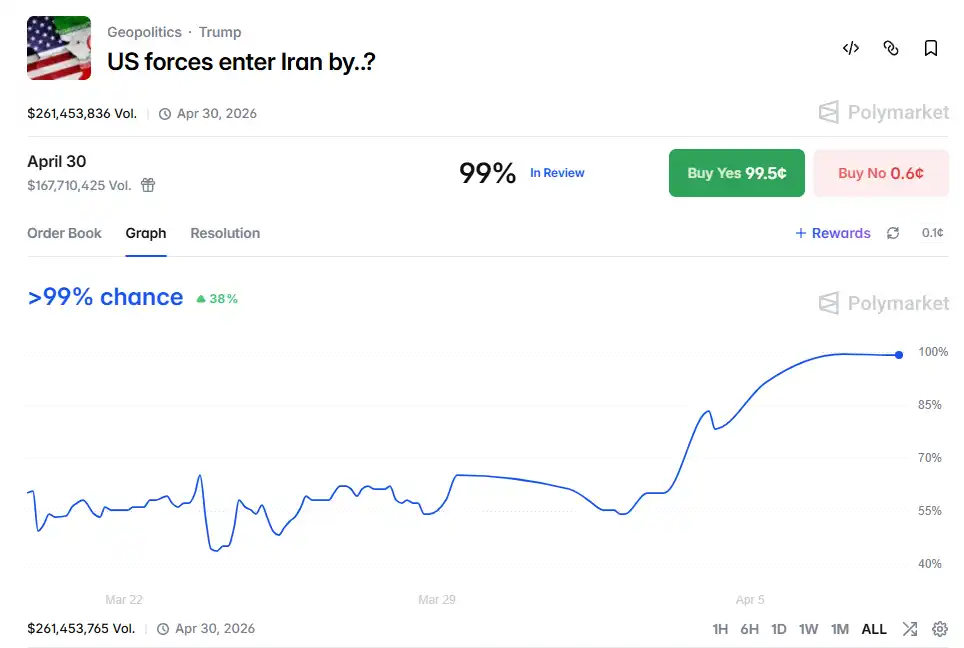

Polymarket: U.S. Rescue of American Pilot in Iran Determined as U.S. Invasion of Iran

On April 3, a U.S. F-15E Strike Eagle fighter jet was shot down by the Iranian air defense system in southwestern Iran. Two crew members (one pilot, one weapon systems officer/WSO) parachuted out, with one quickly rescued and the other missing for several days, hiding in the Iranian mountains.

The U.S. military then launched a search and rescue (SAR) operation, involving armed aircraft, helicopters, etc., and successfully rescued the second severely injured crew member (Trump personally announced "WE GOT HIM"). The rescue operation involved U.S. military entering Iranian territory (mountain search and rescue, possible ground or low-altitude operations), which raised concerns against the current backdrop of sensitive geopolitical conflicts.

As the U.S. military entering Iranian territory can be considered to some extent as a U.S. invasion of Iran, it directly affected the prediction event on the Polymarket platform regarding when the U.S. military would invade Iran (US forces enter Iran by?).

According to the settlement rules, active-duty U.S. military personnel (including special operations forces) entering Iranian land territory before a specified date would be considered an invasion, with the downed pilot not counting as an invasion, but U.S. special forces did indeed enter Iranian territory to rescue the pilot. Therefore, the special forces entering Iran to rescue the pilot met the standard for determining the U.S. invasion of Iran as Yes on Polymarket.

The "Pilot Rescue" event has been judged by Polymarket as the U.S. invasion of Iran, sparking strong community controversy.

Supporters of the "Count as Entry" (Yes side) believe that this action meets the definition of "entry" as per the rules. The U.S. Special Forces actively entered Iranian territory to carry out a mission, and the rules explicitly state that "special operation forces will qualify," including "for operational purposes (including humanitarian)." From an objective standpoint, this is the first confirmed U.S. ground penetration behavior in the current conflict context, with U.S. personnel indeed stepping on Iranian soil, hence should be considered an "entry."

Opponents of the "Count as Entry" (No side) argue that this definition is overly broad. They believe that this action was essentially a short-term, limited humanitarian rescue operation, not an invasion or occupation, and does not align with the general understanding of the public regarding "U.S. troops entering Iran."

Furthermore, the rules explicitly exclude that "pilots who are shot down... will not qualify," and this action revolves around the downed pilot, having the nature of "forced entry," which logically should fall into a similar exception category. Referring to past cases (such as similar regional actions not being considered invasions), rescue actions should not be equated with military entry; if judged as Yes, it may encourage marginal interpretations of the rules, weakening the seriousness and consistency of the market.

The Chinese community also generally believes that "entering Iran" should more specifically refer to large-scale ground or amphibious operations, rather than short-term actions of "rescue and leave."

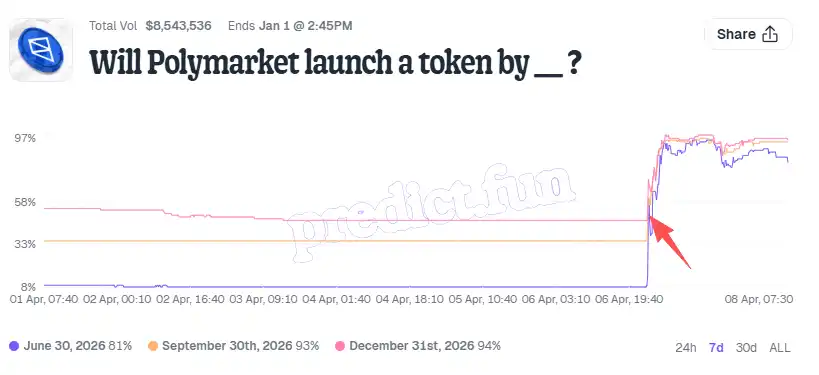

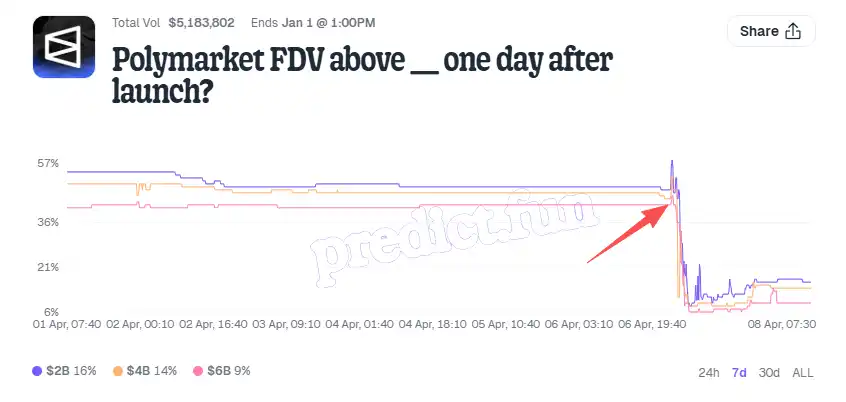

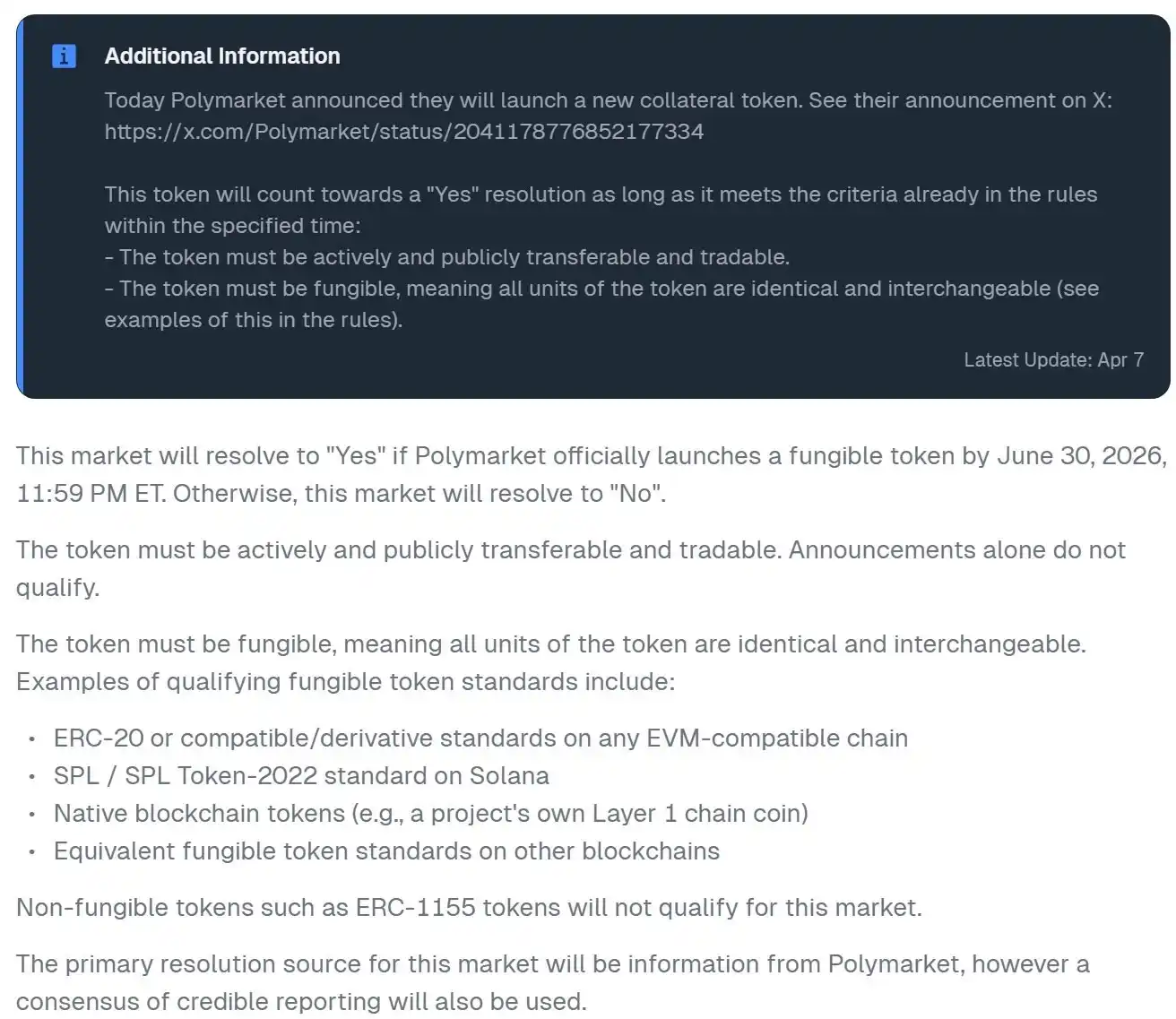

Predict.fun: Polymarket Issuing Stablecoin Deemed as Token Launch

On the evening of April 6, Polymarket officially announced on X that it would undergo a comprehensive platform upgrade:

Rebuilding the trading engine, upgrading smart contracts; introducing a new native collateral token, Polymarket USD (1:1 pegged to USDC, to replace USDC.e, reducing bridging risks).

Notably, the second point mentioned the launch of the native collateral token Polymarket USD, directly impacting the probabilities of two related prediction events on Predict.fun.

One is token launch; the other is post-launch market cap:

1. When will Polymarket launch a token (Will Polymarket launch a token by ___ ?).

2. One day after opening, what was the FDV of Polymarket (Polymarket FDV above ___ one day after launch?)?

According to the settlement rules document, it is clearly stated that "any fungible token issued by Polymarket counts as 'issuance' for this event," and stablecoins are no exception. Therefore, Polymarket's stablecoin meets the criteria to be judged as Yes.

Settlement Rules Explanation

The community has engaged in a debate on this matter.

Supporters argue that based on the literal interpretation of the rules, "token issuance" is not limited to being a "governance token," but is a general reference to all tokens. Under this premise, Polymarket USD, as an ERC20/SPL fungible token issued by Polymarket, fundamentally meets the definition of "issuance." Furthermore, subsequent official clarifications are more of a reiteration of the original rules rather than a temporary rule change, making them somewhat reasonable in terms of compliance.

However, skeptics do not accept this explanation. On the one hand, they believe that including stablecoins in the category of "issuance" is an overinterpretation of the rules and a typical play on words. On the other hand, even if stablecoins are considered "issuance," the core of this prediction market is still the "Polymarket FDV," not the "Polymarket USD FDV." Stablecoins serve more as collateral or settlement tools, and their market value structure differs fundamentally from that of the project's native token (such as the POLY governance token), so they should not be directly equated or substituted for the overall project valuation logic.

Whose Side Are You On?

Overall, the controversial event in the prediction market actually revolves around a central question: are you betting on "reality" or on "rules"? Many times, these two do not completely overlap.

For those of us involved in prediction markets, understanding the rules themselves may be more important than predicting the outcome. How the information source is defined, whether there are any exceptions, whether there is room for interpretation—these details can directly determine the outcome at critical moments.

It is also for this reason that some high-probability events that appear to be a "financial management trap" may not be without risk, but may instead be a potential "loss trap." Many reversals occur precisely in these overlooked details. Instead of blind betting, take a closer look at the rules. It is more useful to do so than to complain after losing money.

You may also like

Consumer-grade Crypto Global Survey: Users, Revenue, and Track Distribution

Prediction Markets Under Bias

Stolen: $290 million, Three Parties Refusing to Acknowledge, Who Should Foot the Bill for the KelpDAO Incident Resolution?

ASTEROID Pumped 10,000x in Three Days, Is Meme Season Back on Ethereum?

ChainCatcher Hong Kong Themed Forum Highlights: Decoding the Growth Engine Under the Integration of Crypto Assets and Smart Economy

Why can this institution still grow by 150% when the scale of leading crypto VCs has shrunk significantly?

Anthropic's $1 trillion, compared to DeepSeek's $100 billion

Geopolitical Risk Persists, Is Bitcoin Becoming a Key Barometer?

Annualized 11.5%, Wall Street Buzzing: Is MicroStrategy's STRC Bitcoin's Savior or Destroyer?

An Obscure Open Source AI Tool Alerted on Kelp DAO's $292 million Bug 12 Days Ago

Mixin has launched USTD-margined perpetual contracts, bringing derivative trading into the chat scene.

The privacy-focused crypto wallet Mixin announced today the launch of its U-based perpetual contract (a derivative priced in USDT). Unlike traditional exchanges, Mixin has taken a new approach by "liberating" derivative trading from isolated matching engines and embedding it into the instant messaging environment.

Users can directly open positions within the app with leverage of up to 200x, while sharing positions, discussing strategies, and copy trading within private communities. Trading, social interaction, and asset management are integrated into the same interface.

Based on its non-custodial architecture, Mixin has eliminated friction from the traditional onboarding process, allowing users to participate in perpetual contract trading without identity verification.

The trading process has been streamlined into five steps:

· Choose the trading asset

· Select long or short

· Input position size and leverage

· Confirm order details

· Confirm and open the position

The interface provides real-time visualization of price, position, and profit and loss (PnL), allowing users to complete trades without switching between multiple modules.

Mixin has directly integrated social features into the derivative trading environment. Users can create private trading communities and interact around real-time positions:

· End-to-end encrypted private groups supporting up to 1024 members

· End-to-end encrypted voice communication

· One-click position sharing

· One-click trade copying

On the execution side, Mixin aggregates liquidity from multiple sources and accesses decentralized protocol and external market liquidity through a unified trading interface.

By combining social interaction with trade execution, Mixin enables users to collaborate, share, and execute trading strategies instantly within the same environment.

Mixin has also introduced a referral incentive system based on trading behavior:

· Users can join with an invite code

· Up to 60% of trading fees as referral rewards

· Incentive mechanism designed for long-term, sustainable earnings

This model aims to drive user-driven network expansion and organic growth.

Mixin's derivative transactions are built on top of its existing self-custody wallet infrastructure, with core features including:

· Separation of transaction account and asset storage

· User full control over assets

· Platform does not custody user funds

· Built-in privacy mechanisms to reduce data exposure

The system aims to strike a balance between transaction efficiency, asset security, and privacy protection.

Against the background of perpetual contracts becoming a mainstream trading tool, Mixin is exploring a different development direction by lowering barriers, enhancing social and privacy attributes.

The platform does not only view transactions as execution actions but positions them as a networked activity: transactions have social attributes, strategies can be shared, and relationships between individuals also become part of the financial system.

Mixin's design is based on a user-initiated, user-controlled model. The platform neither custodies assets nor executes transactions on behalf of users.

This model aligns with a statement issued by the U.S. Securities and Exchange Commission (SEC) on April 13, 2026, titled "Staff Statement on Whether Partial User Interface Used in Preparing Cryptocurrency Securities Transactions May Require Broker-Dealer Registration."

The statement indicates that, under the premise where transactions are entirely initiated and controlled by users, non-custodial service providers that offer neutral interfaces may not need to register as broker-dealers or exchanges.

Mixin is a decentralized, self-custodial privacy wallet designed to provide secure and efficient digital asset management services.

Its core capabilities include:

· Aggregation: integrating multi-chain assets and routing between different transaction paths to simplify user operations

· High liquidity access: connecting to various liquidity sources, including decentralized protocols and external markets

· Decentralization: achieving full user control over assets without relying on custodial intermediaries

· Privacy protection: safeguarding assets and data through MPC, CryptoNote, and end-to-end encrypted communication

Mixin has been in operation for over 8 years, supporting over 40 blockchains and more than 10,000 assets, with a global user base exceeding 10 million and an on-chain self-custodied asset scale of over $1 billion.

$600 million stolen in 20 days, ushering in the era of AI hackers in the crypto world

Vitalik's 2026 Hong Kong Web3 Summit Speech: Ethereum's Ultimate Vision as the "World Computer" and Future Roadmap

On the same day Aave introduced rsETH, why did Spark decide to exit?

Full Post-Mortem of the KelpDAO Incident: Why Did Aave, Which Was Not Compromised, End Up in Crisis Situation?

After a $290 million DeFi liquidation, is the security promise still there?

ZachXBT's post ignites RAVE nearing zero, what is the truth behind the insider control?